Smart Ways to Pay: A Guide to AC Installation Financing

Need a new AC? Discover easy ways for financing AC installation. Compare options & make an informed choice for your home comfort. Apply today!

Why Understanding Your AC Financing Options Matters

Financing AC installation is a practical solution that allows homeowners to upgrade or replace their air conditioning system without depleting their savings. When summer heat hits and your AC fails, you need immediate comfort— but the average cost of a new system can range from several thousand to over ten thousand dollars. Instead of delaying a necessary upgrade or draining your emergency fund, financing spreads this significant expense into manageable monthly payments.

Quick Answer: Key AC Financing Options

- HVAC Company Financing – Often includes 0% APR promotional offers; convenient application through your installer

- Personal Loans – Unsecured loans with fixed rates and flexible terms (typically 1-12 years)

- Home Equity Loans/HELOCs – Lower interest rates using your home as collateral

- Credit Cards – Suitable for smaller projects or those with high credit limits and low rates

Most lenders require a credit score of 600 or higher, though some programs accommodate lower scores. Financing can cover the entire project—both equipment and labor—and modern high-efficiency systems can save up to 36% on annual cooling bills, helping offset the cost of your monthly payments.

As one HVAC contractor noted, “Everybody in home improvement should offer financing” because it makes essential home comfort accessible when families need it most, not just when they’ve saved enough cash.

This guide will walk you through each financing option, explain the application process, and help you identify ways to reduce your total cost through rebates and tax credits. Whether your system just failed or you’re planning a proactive upgrade, understanding your financing choices puts you in control of both your comfort and your budget.

Understanding Your Options for Financing AC Installation

When your air conditioner quits on the hottest day of summer, the last thing you need is financial stress. The good news? You have several solid paths for financing AC installation, each with its own advantages. Choosing a financing option is like picking the right tool for a job—what works for your neighbor might not be the best fit for you. Let’s walk through your main options so you can make a choice that keeps both your home and your wallet comfortable.

HVAC Company Financing

Many HVAC companies—including us at Stafford Heating, Cooling, Plumbing & Electrical—work with trusted lending partners to offer financing programs designed for home comfort projects. This allows you to arrange everything directly through your installer, saving you from shopping around at banks.

The main appeal is convenience and special promotional offers, such as 0% APR for a set period. These offers mean you pay no interest if you stick to the payment schedule. Financing can be bundled right with your AC Installation, covering both equipment and labor in one package.

However, you need to pay close attention to those attractive 0% APR promotions, as they often come with deferred interest. This means if you don’t pay off the entire balance before the promotional period ends, you could be charged all the interest that has accumulated since day one, often at high rates of 28% or even 30%. It’s not a trap, but it requires discipline.

Promotional rates usually require good credit (a FICO score of 690 or higher), but options often exist for those with lower scores, albeit with less favorable terms.

Want to explore what we offer? You can find more info about our financing options on our website. We believe in being upfront and helping you understand exactly what you’re signing up for.

Personal Loans

A personal loan is a versatile and straightforward option. You borrow a lump sum from a bank, credit union, or online lender and repay it in fixed monthly installments over a set period, typically one to twelve years.

The beauty of personal loans is their flexibility. You’re not locked into a specific HVAC company’s lending partner, which gives you more control to shop for the best rate. Most personal loans come with fixed interest rates, so your monthly payment never changes, making budgeting simple.

Another advantage is that these are unsecured loans, meaning you don’t put your home up as collateral. If you struggle with payments, your credit score will be affected, but you won’t risk losing your house.

The trade-off is that because there’s no collateral, lenders charge higher interest rates than for secured loans. Your credit score is the primary factor in determining your rate. You’ll also face a hard credit inquiry when you apply, and some lenders charge origination fees that are deducted from your loan amount.

Curious about how personal loans work in detail? What is a personal loan? offers a thorough explanation.

Home Equity Options (Loans & HELOCs)

If you’ve built up equity in your home, you may have access to one of the most affordable financing options. Home equity loans and Home Equity Lines of Credit (HELOCs) let you borrow against the value you’ve accumulated in your property.

The headline benefit is lower interest rates. Because your home serves as collateral, lenders feel more secure and pass those savings on to you. For a large expense like a new AC system, lower rates can mean significant savings.

There’s also a potential tax benefit: when you use a home equity loan for home improvements (like a new AC), the interest you pay might be tax-deductible. Consult a tax professional to see if this applies to you.

A home equity loan provides a lump sum upfront with fixed monthly payments. A HELOC works more like a credit card, with a credit limit you can draw from as needed during a “draw period.” This flexibility is useful for multiple home improvement projects.

However, your home is the collateral. If you can’t make payments, you could face foreclosure. The application process also takes longer and often involves an appraisal, more documentation, and closing costs. HELOCs also typically have variable interest rates, meaning your payment could rise.

Want to understand the nitty-gritty details? The Consumer Financial Protection Bureau offers a helpful guide: Understanding home equity loans.

The right choice for financing AC installation depends on your credit, home equity, and how quickly you need to act. The key is matching the option to your circumstances.

The Application Process: From Qualification to Approval

You’ve explored your options and found a financing path that seems right. Now comes the practical part: applying. The good news is that it’s more straightforward than you might think. Understanding what lenders look for can turn an intimidating process into a confident step toward a cooler home.

How HVAC Financing Programs Work

Financing AC installation works like most other loans: a lender provides the money upfront, and you pay it back over time with interest. What makes HVAC financing helpful is that it’s designed specifically for home comfort projects.

Financing typically covers your entire project cost—not just the AC unit, but also installation labor, ductwork adjustments, and removal of your old system. Everything gets rolled into one manageable package. Most programs offer repayment terms between 1 and 10 years, giving you the flexibility to choose a monthly payment that fits your budget.

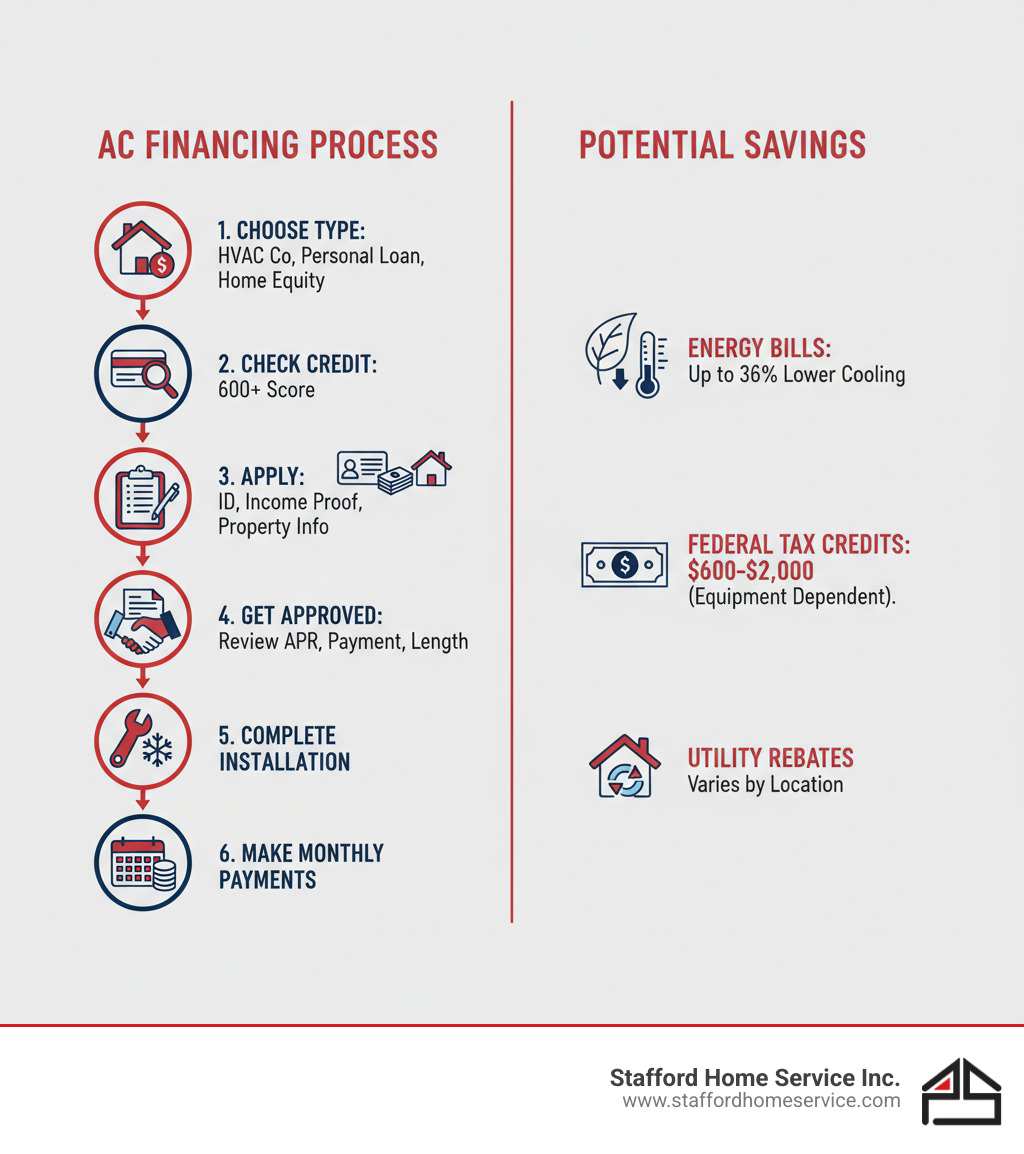

Qualifying for Financing AC Installation

Your credit score is the most important factor for lenders. Most want to see a score of 600 or higher to approve you for financing AC installation. If you’re aiming for promotional offers like 0% APR, you’ll typically need a score of 690 or above.

Even if your credit isn’t perfect, you still have options. Some programs work with homeowners who have scores as low as 500, though these usually come with higher interest rates.

Lenders also examine your debt-to-income ratio—your total monthly debt payments compared to your gross monthly income. A lower ratio shows you’re in a stronger position to handle a new loan.

Applying for financing will result in a hard inquiry on your credit report, which might temporarily lower your score. However, making consistent, on-time payments helps build your credit over time.

What to Expect When You Apply

The application process has become surprisingly simple. Before you start, gather your government-issued photo ID, proof of income (like recent pay stubs or tax documents), and possibly your property tax information.

Many lenders offer quick online applications where you can check for pre-qualified offers without impacting your credit score. Within minutes, you can see what offers you qualify for, including interest rates, monthly payments, and loan terms.

This is your chance to compare. Don’t feel pressured to accept the first offer. Look at the APR, the loan term, and the monthly payment to ensure it fits your budget.

The approval timeline varies. Online lenders often provide rapid decisions, sometimes the same day. Home equity options typically take longer—from several days to a few weeks—due to more extensive documentation. Once approved, funds can be disbursed quickly so your installation can proceed.

At Stafford Heating, Cooling, Plumbing & Electrical, we work to make this process as smooth as possible. We’ve partnered with trusted lenders to offer financing that covers both equipment and labor, so you can focus on enjoying your cool, comfortable home.

Maximizing Value: Rebates, Tax Credits, and Smart Comparisons

Securing financing for your AC installation is just the first step. The real win comes from combining smart financing with every available incentive to reduce your total investment. Think of it as a one-two punch: manageable monthly payments plus immediate savings.

Opening Savings with Rebates and Tax Credits

The government encourages homeowners to upgrade to energy-efficient AC systems, and they’re willing to help you pay for it. When you choose a high-efficiency central air conditioning system, you can save up to 36% on your annual cooling bills.

The Inflation Reduction Act of 2022 created substantial opportunities for homeowners. For qualifying systems installed by December 31, 2025, you could receive federal tax credits that significantly offset your costs. A qualifying standalone air conditioner might earn you up to $600, while an AC and furnace combo could qualify for up to $1,200. Heat pumps offer even more generous credits—up to $2,000. The maximum you can claim annually is $3,200 when combining various credits.

These are tax credits, not deductions, meaning they directly reduce what you owe the IRS. It’s always smart to consult with a tax professional to understand how these apply to you.

Beyond federal programs, your local utility company may offer its own rebates for energy-efficient HVAC installations. These vary by location but can add hundreds more to your savings. We can help you identify what’s available, or you can explore options on our “Rebates & Tax Credits” page. The Home Energy Rebates Programs website also provides comprehensive information.

How to Choose the Best Plan for Financing AC Installation

With multiple financing paths and incentives available, how do you choose the right combination? It comes down to a few key factors.

- Start with the Annual Percentage Rate (APR). This number tells you the true cost of borrowing. Even a small difference can translate into hundreds of dollars over the life of your loan.

- The loan term is also important. A shorter term means higher monthly payments but less total interest paid. A longer term brings lower monthly payments but accumulates more interest. Choose what fits your budget while minimizing your total cost.

- Always calculate the total cost you’ll repay over the entire loan period. This is the real price tag for financing AC installation.

- Watch out for hidden fees like application or origination fees. Also, check for prepayment penalties, as the best options let you pay off your loan early without extra charges.

- If you’re considering a promotional 0% APR offer, understand how deferred interest works. If you don’t pay off the entire balance before the promotional period ends, you could be hit with all the interest that would have accrued from day one. Be honest with yourself about whether you can pay off the full amount in time.

- Your credit score will determine which options are available and at what rates. A higher score opens doors to better terms.

Here’s a practical comparison to help you see the differences at a glance:

At Stafford Heating, Cooling, Plumbing & Electrical, we believe in transparency. That’s why we offer straightforward financing options and help you understand all available incentives.

Frequently Asked Questions about AC Financing

We hear from homeowners every day who have questions about financing AC installation and repairs. Here are some of the most common concerns we address at Stafford Heating, Cooling, Plumbing & Electrical

Can I get financing for AC repairs as well as installation?

Yes, absolutely. Financing isn’t just for brand-new system installations. Many financing programs are designed to cover the full spectrum of Air Conditioning Services in Minneapolis MN, including major repairs and component replacements.

Whether your compressor needs replacing or you’re facing other repairs, financing can help you spread those costs into manageable monthly payments. This is especially valuable for unexpected failures when you need comfort restored immediately. Ask your HVAC provider what their financing programs cover.

How does deferred interest work on promotional financing offers?

This is a critical detail for any “0% APR” or “same-as-cash” offer. With deferred interest, interest accrues from the purchase date but is waived if you pay off your entire balance before the promotional period ends.

However, if even a small balance remains after the deadline, you will be charged all the retroactive interest on the full original loan amount, often at a very high APR (28-30%). That attractive deal can become very expensive. Only choose a deferred interest promotion if you are confident you can pay off the entire balance before the window closes. Otherwise, a traditional loan with a fixed APR might be a safer choice.

Is it better to replace my furnace and AC at the same time?

For many homeowners, the answer is yes—especially if both systems are aging. While it’s a higher upfront investment, the benefits often outweigh the cost.

- Matched System Efficiency: Modern HVAC systems are engineered to work together. Pairing a new, high-efficiency AC with an old furnace can reduce its efficiency and limit your energy savings.

- Long-Term Savings: A fully matched, high-efficiency system delivers maximum energy savings on your utility bills for years to come.

- Less Disruption: Replacing both systems at once means just one installation appointment and avoids another major project when the second unit fails soon after.

- Bundled Financing and Discounts: You can often roll both the furnace and AC into a single financing plan. Some contractors even offer discounts when you purchase both units together.

If your furnace is 15 years or older and your AC is also approaching the end of its lifespan (10-15 years), replacing both is usually the smart move. We always recommend consulting with an HVAC professional to assess your specific situation.

Conclusion: Make a Cool and Confident Decision

When your AC gives out on the hottest day of summer, the last thing you should worry about is how you’ll afford the replacement. That’s where financing AC installation truly shines—it transforms a potentially overwhelming expense into manageable monthly payments, letting you enjoy immediate comfort without emptying your savings account or putting off a necessary upgrade.

Throughout this guide, we’ve walked through your main options: the convenience of HVAC company financing with attractive promotional offers, the flexibility of personal loans, and the potentially lower rates of home equity options. Each path has its strengths, and the right choice depends on your credit score, how quickly you need approval, and whether you’re comfortable using your home as collateral.

But financing is just one piece of the puzzle. Don’t leave money on the table—take full advantage of federal tax credits for energy-efficient systems and check with your local utility company for rebates. These incentives can significantly reduce your total investment. And here’s a crucial reminder: if you’re considering a 0% APR promotional offer, make absolutely certain you can pay off the balance before the promotional period ends. Deferred interest can turn what seemed like a great deal into an expensive surprise.

At Stafford Heating, Cooling, Plumbing & Electrical, we believe that quality home comfort shouldn’t be out of reach. We’re committed to quality workmanship and complete customer satisfaction, which is why we offer clear, straightforward financing options. Your peace of mind matters to us, and we’re here to help you steer every step—from choosing the right system to finding the financing that works for your budget.

Ready to take the next step toward a cooler, more comfortable home? Don’t wait for the next heat wave to make your move. Schedule your HVAC service in Minneapolis today, and let’s find the solution that’s right for you.

Customer Testimonials

Our customers consistently praise our knowledgeable technicians, prompt service, and the lasting quality of the work we deliver.